You are Going to Die! Philanthropy 3.0 – Your New Wealth Planning Strategy

February 7, 2019 | Blog

They say that nothing is certain except death and taxes. Since those two things are inevitable, what can be done to make them less stressful? This is where Philanthropy 3.0 comes in. As a planning tool, Philanthropy 3.0 can work towards wealth management, tax planning and establishing a living legacy that can be an emotional comfort for your friends, family and community upon your passing.

In an earlier post, Financial Literacy & Philanthropy, we shared some ideas around values based wealth planning; moving from a pyramid model to a values based financial plan. Instead of leaving legacy planning to the end of your wealth creation days, you put legacy planning at the front. This allows you to create a values-centred wealth strategy.

This post looks at how you apply the concepts of tax and wealth planning to creating a living legacy. Specifically looking at the inter-generational conversations and how to engage your advisors in meaningful conversations about philanthropy, legacy, and impact investing.

The Philanthropy 3.0 Discussion – Say What???

Consider the conversations you have with your financial advisors. Usually they are around your retirement planning, saving for your kids’ education, investment strategies to maximize your wealth and ways to capitalize on tax loopholes.

Through some work done with the Purposeful Planning Institute members, we found that while over 70% of High Net Worth (HNW) and Ultra High Net Worth (UHNW) Advisors say they talk to their clients about philanthropy and legacy, only 20% of their clients said that those same advisors actually spoke to them about philanthropy. Why this disconnect? In large part it has to do with the motivation and context of the conversation. What was pointed out was that the clients heard “tax planning” and the advisors thought they were talking “philanthropy.”

This approach to wealth management and tax planning has changed…

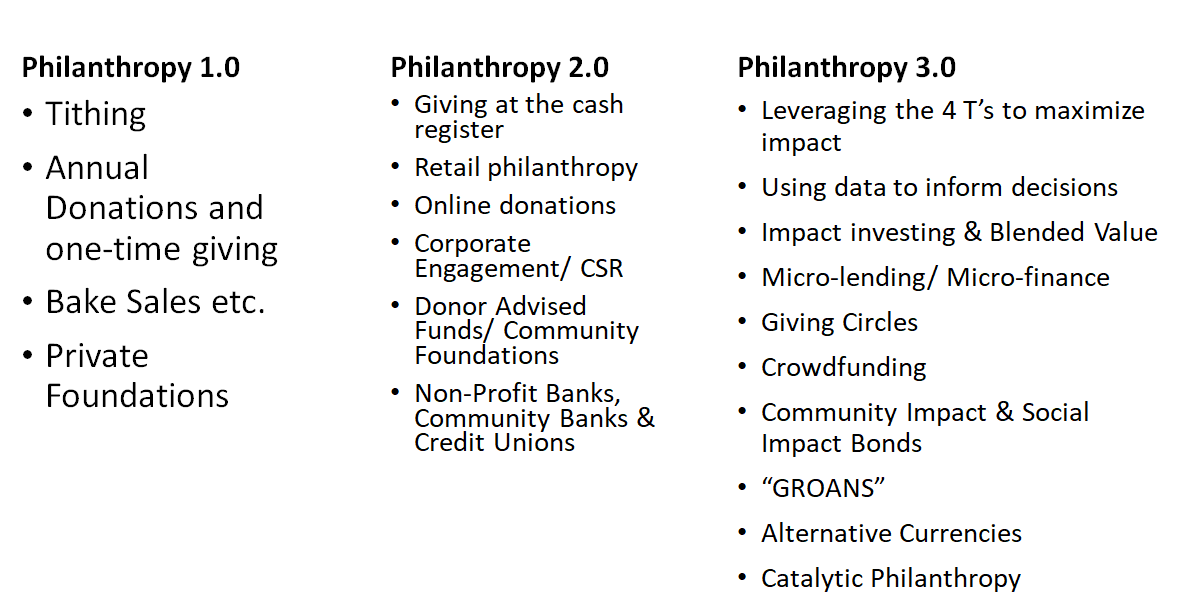

In a Philanthropy 3.0 context we remove the bifurcated approach of financial planning between wealth creation and social change. In this new model of wealth management you don’t break out your wealth creation from your charitable giving. You don’t separate your tax planning from your legacy planning. You don’t divide your investment strategy between impact investments and regular investments. Philanthropy 3.0 combines your consumer behaviour, your charitable inclinations, your lifestyle spending and your financial planning strategy into one comprehensive approach to wealth management.

Gone are the days when impact investing meant patient capital and private equity only. In fact, today, many impact funds are RRSP and RESP eligible. According to research on Impact Investing published in 2018 by MaRS, impact investments out-perform traditional markets by 5.5%. It is expected that by 2020 over $300B will be invested in social purpose business and impact funds globally.

The Evolution from Philanthropy 1.0 to Philanthropy 3.0

It is the time of year when we sit down to plan out our RRSP and 401K contributions. We will determine what will get put into our TFSA and RESPs, and manage the tax issues that were realized in 2018 and looking into 2019. When you overlay Philanthropy 3.0 onto your financial planning you two things will be realized:

- You will be able to capitalize on tax incentives in the near future

- Your legacy will be coordinated within your financial growth strategy. This means that while you are growing your wealth you are also focusing on generating social capital.

What results is a way for you to have the types of conversations with your inheritors, your advisors and other stakeholders that will ensure your plan is actualized when you are no longer around to inform the decision makers.

Up to Six Generations Influencing your Wealth & Legacy Plan

“Legacy is more than your mother’s pearls, it is about her pearls of wisdom.”

Financial planning conversations can be tricky. Money is a taboo topic. With this taboo comes a cloak of secrecy which can feed into distrust between family members. A Philanthropy 3.0 approach bridges some of the communication gaps that occur around taboo topics and generational divides.

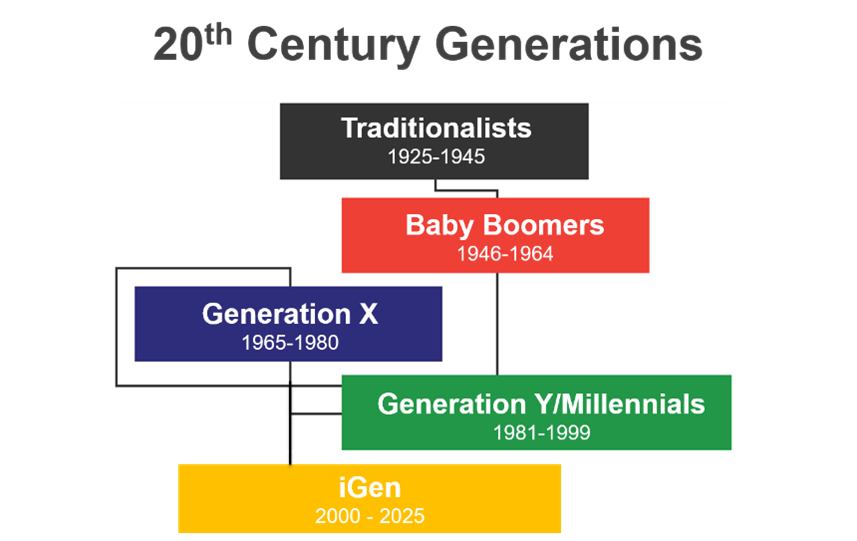

Currently, at the wealth planning table in North America there are up to six generations. Individuals who were born around the Great Depression (1930’s) – we call them Traditionalists. Baby Boomers who were born between World War II and the Vietnam War (Hippies who became Yuppies). Gen Xers who comprise the Disco Era and Microwave Generation. Gen Yers are children of Baby Boomers and Gen Xers (depending on how long people waited to have kids). Millenials are blended with GenY as it depends on the generation of their parents (either Boomers or Xers). The Millenials are now entering the workforce and grew up where everyone was an MVP on their soccer team. Lastly, we have the iGen – those who are born after 2005 and will continue to be born until 2025.

For the first time the younger three generations may have parents that are not just a single generation older, but in some cases two generations older. This generational make-up means that the traditional nuclear family is no longer the financial model for families. A new family dynamic is influencing the family wealth models. These new family wealth models are not only built upon the number of generations who have a voice at the table, but also their perspectives of wealth is shaping the discussion. (Image source: Johnson Centre for Philanthropy and 21/64).

For example, the GenY folks look at philanthropy in “off-book” ways. Meaning they are just as likely to support a cause through Go Fund Me, which is not a registered charity, as they are to support a volunteer project tied to an experience provided by a large-scale social enterprise like “We Day.”

Attitudes Towards Wealth

By considering what shapes the different generations’ attitudes towards wealth you can establish a financial plan that reflects your values from all perspectives of on wealth:

- Consumer behaviour – What we buy (or choose not to buy); when we buy it, what we use to make purchases (credit, cash, bitcoin, alternative currencies); how we buy it (online, in person, through a broker, barter, consignment, memberships); types of businesses we choose to support (local, multi-national, big box, artists, sole proprietors, social ventures, etc.)

- Investment behaviour – What we invest in (securities, impact funds, property, etc); when we invest in it; why we invest in those things, how our investments align with our purchases and charitable objectives, crowd funding, angel networks, venture capital

- Lifestyle behaviour – Where we choose to live (own, rent, square footage, walkable neighbourhoods); how we transport ourselves (car, car-share, bike, public transit, walk); where and how we vacation

- Philanthropic behaviour – Where we deploy our capital (local, national, international); how we fund projects (direct, through a giving vehicle like a Donor Advised Fund or community foundation, or through a third party like United Way); when we deploy these funds (when we are alive, upon death, to commemorate a special event); why we are doing this (specific issue you want to address, personal relationship with an organization or the person who asks, change that you want to see); the types of charities that are supported (start-ups, institutions, size, etc.)

Before you sit down with your accountant and financial advisor to talk about your upcoming tax strategy, consider how you are influencing the wealth conversation between generations. Are there areas that you can hone in on to demonstrate your values? Can you bring your advisors into the conversation to help you craft the messages you want to convey to those whom will be affected by your wealth planning?